The Great Wealth Transfer

Over the next two decades, an estimated $84 trillion will transfer from the Silent Generation and Baby Boomers to younger generations, in what economists call the Great Wealth Transfer.1 This shift is reshaping how families think about financial planning.

Foundational Shifts

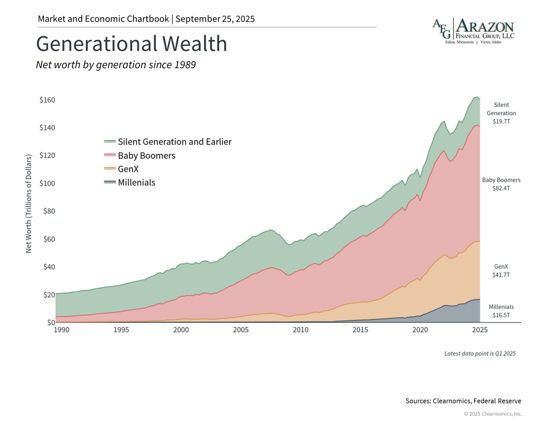

The size and structure of wealth transfers have evolved over the past few decades. Baby Boomers, those between 61 and 79 years old in 2025, now hold over $82 trillion in wealth according to the Federal Reserve. Not only did a transformation from pension plans to liquid retirement accounts place the onus on retirees to save enough and manage their retirement funds appropriately, but - in successfully doing so - these generations are now faced with an equally formidable task: how to transfer wealth in the most meaningful and tax-efficient ways. Thus, the Great Wealth Transfer represents both opportunity and responsibility.

Why Navigating the Great Wealth Transfer Matters

What makes this particularly important is that these assets often represent decades of disciplined saving and investing. Today's wealth transfers frequently involve diversified investment portfolios, multiple retirement accounts, and various tax-advantaged savings vehicles. On top of inherited real estate or family businesses that previous generations might have passed down, each of these requires careful planning to ensure smooth transitions and optimal tax treatment.

Wealth Transfer planning is a process as dynamic as any other part of financial planning. General circumstances, increased level of wealth, and family dynamics play a role and can reshape your intentions around the transfer of your wealth. And on top of this, changes in tax law and legal structures can shake up what may have previously seemed like the right set of tools to carry out those intentions, creating the need to make a number of adjustments to your plan at any given time.

Combining the Right Tools

Turning to actionable strategies, some of the most important decisions in optimizing a wealth transfer involve timing and taxes. Here are just a few impactful strategies to consider:

- Tax-Efficient Lifetime Giving. Giving during your lifetime isn't appropriate for everyone; It requires confidence that you won't need the gifted assets for your own retirement security. That being said, annual gift tax exclusions allow an individual to transfer up to $19,000 per recipient in 2025 without reducing your lifetime estate tax exemption. And, lifetime giving can provide benefits beyond tax savings, as you can take part in how beneficiaries receive, place purpose to, and manage the money you give them. This has meaningful ripple effects.

Those who are interested in charitable giving also have access to a number of tools, including Donor Advised Funds and Qualified Charitable Deductions (QCDs) from retirement accounts, to name a couple.

- Multigenerational Education Funding. By investing in education, you can provide young family members with the tools and knowledge needed to build successful futures.

Unlike other gifts, payments made directly to educational institutions for tuition don't count against annual gift tax exclusions. Additionally, contributions to 529 education savings plans offer unique benefits for legacy planning, as you can contribute substantial amounts while retaining control over the account. 529s can be used for K-12 tuition, college, and even student loan repayments. Enactment of recent legislation further validates the multifaceted capabilities of 529s, allowing for beneficiaries of these accounts to roll over up to $35,000 from 529 funds to Roth IRAs under qualifying circumstances.

For larger families with multiple grandchildren or great-grandchildren, education trusts may also be considered. While education trusts can add complexity, they can also help ensure equitable treatment across beneficiaries, supporting multigenerational family members over time and creating an enduring legacy.

- Asset Location Strategies. Asset location involves strategically placing investments within different account types - taxable, tax-deferred, and tax-free - aiming to maximize outcomes.

By thoughtfully considering your financial structures and mapping certain assets to certain bequests, you can seek to ensure you and your beneficiaries get the most out of your money. You can even use techniques such as tax-loss harvesting to minimize any tax implications.

For example, if you have large unrealized capital gains in a taxable account, you have options to minimize the tax burden. This might include waiting until after death for the cost basis to “step up,” or potentially deciding to gift that asset to charity over time. If done thoughtfully, gifting could provide the double benefit of upfront tax deductions along with not having to realize the tax on that gain.

- Advanced Estate Planning. As wealth transfer amounts increase and tax implications become more complex, advanced estate planning techniques can also become beneficial.

This might involve trusts that distribute assets over time, including specific provisions or charitable components that involve the next generation. The complexity of modern wealth transfer also extends to business interests, retirement account beneficiary designations, and coordination between different types of liquid and illiquid assets.

All of these strategies require specific expertise to ensure optimal outcomes and avoid unintended consequences. Yet, the opportunity to help future generations succeed has never been brighter.

The bottom line? The Great Wealth Transfer represents a historic opportunity to create lasting impact across generations. If you feel the need to review or discuss your Wealth Transfer plan, our team is poised to have this meaningful conversation with you.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.

Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

- https://www.cerulli.com/press-releases/cerulli-anticipates-84-trillion-in-wealth-transfers-through-2045

- https://www.irs.gov/publications/p590a#en_US_2024_publink1000129982