The Federal Reserve plays a central role in financial markets and the economy, and its importance has only grown in recent decades. From the 2008 global financial crisis to the inflationary period of the past several years, investors have followed every Fed decision carefully. So, when leadership changes occur at the Fed, they naturally capture the attention of investors and the broader public. Now that Kevin Warsh has officially taken office as Fed Chair, these questions have shifted from speculation to real-time policy expectations. At the same time, it’s important to understand what the Fed does and does not control when it comes to long-term investing.

Kevin Warsh, now serving as Fed Chair after confirmation by the Senate, is an experienced policymaker who previously served on the Fed's Board of Governors during the global financial crisis. Markets initially responded favorably to his appointment, viewing him as a known quantity with deep familiarity with monetary policy and financial markets. Early signals from his tenure suggest a steady but disciplined approach, though investors are closely watching how his views translate into policy decisions in a still-uncertain economic environment.

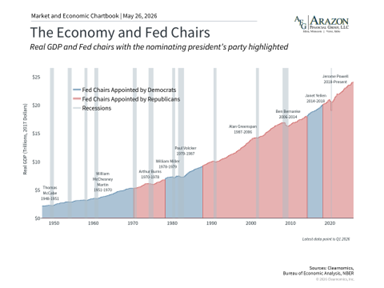

The economy has grown under many Fed leaders

Fed leadership transitions happen infrequently, so it’s helpful to zoom out for perspective. The Chair of the Federal Reserve serves a four-year term, while members of the Board of Governors serve rotating 14-year terms. This structure is designed to separate monetary policy decisions from short-term political pressures, a principle known as “Fed independence,” which continues to be tested in practice.

History shows that the U.S. economy has expanded under a wide range of Fed chairs, regardless of which president appointed them. Paul Volcker, Alan Greenspan, Ben Bernanke, Janet Yellen, Jerome Powell, and now Kevin Warsh have each faced very different economic challenges. These have included stagflation, financial crises, pandemics, and inflationary shocks. In between, the economy has moved through multiple cycles, requiring the Fed to adapt its tools and strategies over time.

Importantly, the Fed and interest rates are only one part of the broader economic picture. The Federal Reserve Reform Act of 1977 established the Fed’s “dual mandate” to promote maximum employment and stable inflation, ideally supporting sustainable long-term growth.

However, despite the attention it receives, the Fed does not control all aspects of the economy. Its primary tools, such as the federal funds rate and balance sheet policy, are often described as blunt instruments that operate with “long and variable lags.” External forces such as geopolitical conflict, energy prices, technological change, and demographic trends continue to play a significant role. For example, while the Fed can respond to inflation driven by higher oil prices or shifts in the labor market due to AI, it cannot directly control those forces.

For investors, this reinforces the idea that focusing too heavily on each Fed decision can obscure the bigger picture. Understanding the broader economic forces at play can help maintain a long-term investment perspective.

Kevin Warsh believes in a more focused Fed

Like all policymakers, Warsh operates without perfect foresight and must rely on evolving economic data. Early in his tenure, he has reiterated his belief in a more focused Federal Reserve, emphasizing a clearer alignment between the Fed’s responsibilities and its actions. He has also strongly reaffirmed the importance of monetary policy independence, even amid ongoing political pressure around interest rates.

Warsh has long been viewed as an inflation hawk, generally favoring tighter policy to ensure price stability. While he has not made abrupt policy changes since taking office, his communications suggest a willingness to keep rates higher for longer if inflation proves persistent. This stance is particularly relevant given recent data showing inflation remaining above the Fed’s 2% target.

For investors, there are several key implications. First, it may take time to fully understand how Warsh’s leadership style will shape policy, especially as he balances market expectations with political realities. Tensions between the Fed and the executive branch are not new, and early commentary suggests that dynamic may continue, particularly if economic growth slows while inflation remains elevated.

Inflation and the money supply complicate Fed decision-making

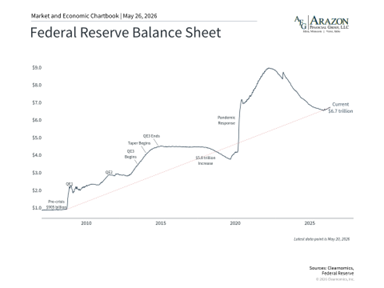

Second, while Warsh believes the Fed has overstepped with green initiatives and social policies, he has not argued for wholesale changes of the core of the institution. Specifically, Warsh believes that crisis-era actions such as the expansion of the Fed’s balance sheet were appropriate, since, after all, he was in the room when many of those decisions were made.

3

Instead, he does believe that the Fed should “retrace its steps” once conditions normalize and the crisis is over. In other words, the Fed’s balance sheet, which remains sizable at $6.7 trillion, is not where it ought to be now that the 2008 financial crisis and the pandemic are long over. In theory, shrinking the balance sheet should tighten financial conditions, since this involves either selling or reinvesting less each month in Treasury securities and mortgage-backed securities. This is often known as “quantitative tightening,” the opposite of the easing done during crisis periods. Changes in this policy can have effects on bond prices, mortgage rates, and corporate borrowing costs.

Third, Warsh believes that Fed policy, especially since the pandemic, has contributed to the growth of the federal deficit and national debt. Just as with the Fed’s balance sheet, he argues that while spending may be justified in recessions, it should be symmetric and monetary policymakers should steer clear of fiscal commentary.

4

Of course, the Fed does not directly control federal spending, and it’s unclear what the new Fed Chair would do differently to influence budgets passed by Congress. To the extent the Fed does weigh in on the size of the budget deficit, it would either be with guidance or by controlling interest rates. For investors, this is another reason that policy rates may continue to depend on many factors in the coming years.

The new Fed Chair inherits a particularly challenging economic environment. Inflation has accelerated in recent months due to higher oil and gasoline prices, driven by the war in Iran. Headline CPI was 3.8% year-over-year as of April 2026, with core CPI at 2.8%, both still above the Fed's 2% target.

This has created a difficult policy backdrop. While many at the Fed and in markets had previously been expecting further rate cuts, fed funds futures now reflect the possibility that the Fed may need to consider a rate increase by early 2027. These market expectations should be taken with a grain of salt, as they shift frequently based on new economic data and global events. Still, they highlight the uncertain path ahead for monetary policy.

For investors, the most important takeaway is that markets and the economy have performed well across many different Fed leadership transitions and policy environments. Changes at the top of the Fed naturally generate uncertainty, but they rarely alter the long-term fundamentals that drive financial markets. Earnings growth, productivity, demographics, and innovation are ultimately the most important drivers of long-run returns.

The bottom line? As Kevin Warsh takes over as Fed Chair, it’s important to maintain perspective on the role of the Fed. Ultimately, understanding the longer-term drivers of the market and economy is the best way to achieve financial goals.

References

- https://www.senate.gov/legislative/LIS/roll_call_votes/vote1192/vote_119_2_00120.htm

- https://www.banking.senate.gov/imo/media/doc/warsh_testimony_4-21-26.pdf

- https://www.wsj.com/opinion/the-high-cost-of-the-feds-mission-creep-role-responsibility-monetary-policy-economy-20a352f8

- Ibid.

Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal professional.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.

This material was prepared by Clearnomics, Inc., who is not affiliated with the named financial professional, firm or broker/dealer.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.